How to Use Business Credit Cards Wisely & Avoid Costly Mistakes

Depending on where you are in your business, using a business credit card may or may not be wise. We’d like to touch on some of the “do’s” and “don’ts” of business credit so you can determine if you are using yours wisely.

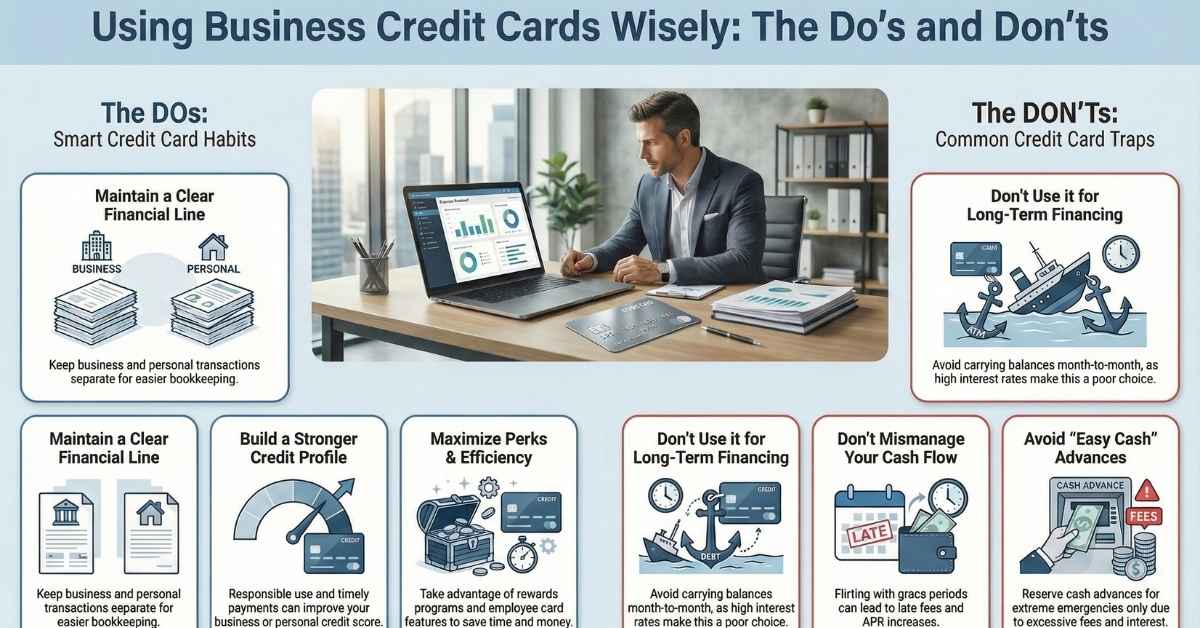

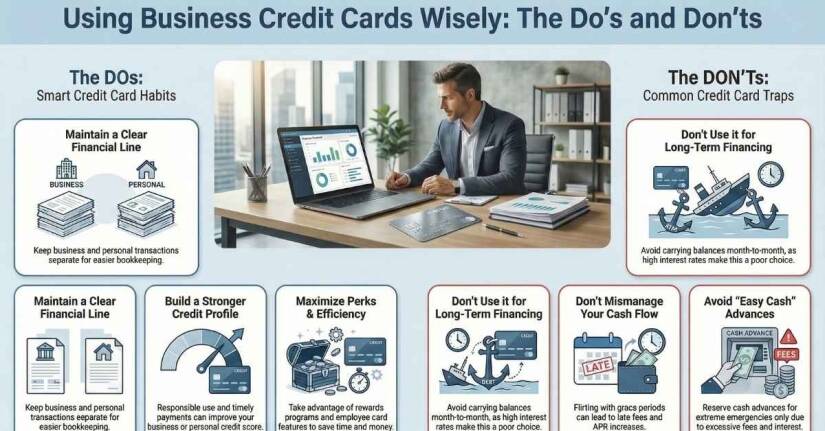

DO

You keep things separated. On this blog we’ve talked about keeping transactions separate and having a business credit card is one of the mechanisms you can use to enable that practice. Use your personal card for personal expenses, your business card for business expenses.

Itemization becomes easier. Many credit card companies’ auto-categorize transactions on monthly statements, which can be a helpful double/cross-check on your bookkeeping. This may catch an accidental miscategorization on your own side, as credit card companies are basing their categorizations on millions of transactions and their categorization is likely to be very accurate.

Credit gets built. Whether the credit card company you use scores it to your personal record or to your business credit, smart management of your card can earn you a better score. It’s always nice to have a business add to your personal life, as it usually requires a lot of sacrifice!

You can use it for your employees. A lot of business cards have the mechanism to allow you to assign cards to employees, which then saves the business (and your staff) time and money when it comes to reconciling and reimbursement. Some companies now have a feature in which cards are turned “on” and “off” via the web so that they are only active for when employees are on trips or are using them.

Rewards. A lot of business cards have rewards – be it miles, points, or even products – so in the rough and tumble of business, it’s nice to get some “free” stuff every now and then. You can use these for yourself or reward employees for hard work. Talk to your tax professional about any possible tax implications.

DON’T

Don’t card hop. If you’re having to transfer balances to take advantage of lower APRs, you are using your credit card for mid to long term financing, which given the rates is not a smart play. Business credit cards should be used for expenses that can be paid off within a month or two – or sometimes for an emergency purpose that might take 6 months. But if you don’t stay with a card company, you won’t have an opportunity to build a relationship, increase your credit line, etc. It will also make things more challenging for your accountant and you don’t want an unhappy accountant, trust us!

Manage your cash flow. Most cards are going to have a 21-day grace period so you don’t have to pay immediately if it’s not right for your cash flow. That being said, don’t flirt with the grace period too much – a late fee or increased APR can totally negate the cash flow benefits it afforded you in the first place. A one-time late fee can sometimes get forgiven if you ask, but only once and then your APR interest also get bumped. Having the right “payment principles” in place will trickle down to how your staff deals with all A/R and A/P.

Cash Advance. Repeat after us: I will only use the cash advance feature in case of extreme emergency. Using it too often will habituate you to “easy cash” which ends up being not so easy when you get your statement and see the fees and APRs associated with this mechanism. Outside of an emergency, it won’t usually make sense to use this feature.

Credit is important in business – whether you are extending it to your customers, or seeking it yourself. Think of it as a finite resource that you have to manage carefully. If you manage it well, it can be an extra component of your business that you can use as a tool to your benefit. Manage it badly, and it will become a terrible source of stress and can have repercussions for your personal credit, not just your business credit.

At Outsourced Bookkeeping, we help you make smarter financial decisions—like when and how to use your business credit card effectively.

About the Author